As Prepared for Delivery

Thank you, Rush, for the kind introduction. And thank you to Mike Froman and the Council on Foreign Relations for hosting me.

Few topics are a greater priority today – for the Biden administration in general and the U.S. Treasury in particular – than our economic engagement with China. Underlying our responsible management of the economic relationship and our goal of a healthy economic competition is the belief that we needed to enhance communication, especially in areas where we disagree – something President Biden made clear after his meeting with President Xi in late 2022. In a speech last year at SAIS, Secretary Yellen laid out three principal objectives for our economic approach to China: first, securing U.S. national security interests and protecting human rights; second, seeking a healthy economic relationship with a level playing field; and third, cooperating in areas where we can and must, such as climate change. As U.S. lead for the Economic Working Group between the U.S. and China, I have spent many hours in discussions with Chinese counterparts toward achieving these three objectives.

Today, I will focus on the second of these objectives: our pursuit of a healthy economic relationship between the U.S. and China with a level playing field for American workers and firms. Such a relationship could be beneficial to both sides. But we are growing concerned that China’s enduring macroeconomic imbalances and non-market policies and practices pose a significant risk to workers and business in the United States and rest of the world. We are worried these features of China’s economy can lead to industrial overcapacity that has significant spillovers around the world and can compromise our collective supply chain resilience given the resulting over-concentration in some manufacturing sectors.

Let me be clear – we remain fully supportive of trade, which obviously includes countries exporting goods they produce. But overcapacity is something different: it is not just production in excess of domestic demand, it is production capacity untethered from global demand.

Overcapacity concerns and interventions are not new – but we are seeing a resurgence of risks in new sectors. Earlier rounds of overcapacity led to job losses in the United States and shuttered American firms. Given China’s size today, spillovers from its economy will be even more consequential.

That is why today I want to discuss what overcapacity is, what Chinese policies cause it, where are we seeing it, the potential global spillovers, and how we should respond.

China’s Macroeconomic Imbalances and Global Spillovers

As an international macroeconomist, I have studied the economic relationship between the United States and China for decades – both as an academic and as a policy official. And throughout this time, perhaps the defining characteristic of this relationship has been macroeconomic imbalances and their effects.

Take, for example, China’s savings rate. China has maintained an exceptionally high savings rate for decades and over the past 20 years it has been roughly 45 to 50 percent of GDP. That is more than twice the historical OECD average and about 10-20 percentage points above comparator East Asian economies. China comprises 28 percent of total global savings, while only 18 percent of global GDP. The corollary of high savings is low levels of household consumption. At less than 40 percent of GDP, China’s consumption is low relative to other countries at similar levels of income.

It is textbook economics that these savings must be channeled somewhere, which leaves the Chinese economy reliant on a combination of domestic investment and foreign demand to drive growth. The mix between these two factors has fluctuated over time. Twenty years ago, China relied on foreign demand and had large growing current account surpluses. In the last decade, Chinese investment in infrastructure and real estate has absorbed much of the savings. But the recent downturn in China’s property sector and the underperformance of its domestic economy raises questions about the drivers of future growth – and, in particular, China’s likely reliance on foreign demand to sustain its growth going forward.

When China relies on foreign demand for growth, and especially when sectoral trade surpluses grow rapidly, the resultant loss of jobs and reduced wages can create lasting and significant damage to individuals and communities around the world, particularly those with low incomes. We are all familiar with the so-called “China shock” that has hit workers and businesses not only in America but across the globe. For example, from 2008 to 2013, China’s push in solar panel manufacturing contributed to an 80 percent decline in international prices and led to bankruptcies and firm closures in the United States and Europe, while Chinese solar output continued to expand on the back of $18 billion in below-market loans.[1] In the steel sector, from 2000 to 2015, China added over eight hundred million tons of steelmaking capacity, and Chinese production volume eclipsed the total volume produced by the rest of the world.[2] When Chinese consumption stalled but production did not, this depressed prices to record lows, reduced utilization rates of foreign steel producers, and contributed to the loss of nearly 100,000 jobs in the U.S alone.[3]

Now, China’s economic size exacerbates this challenge. A 3 percent current account surplus for China today would be almost the same share of global GDP as a 10 percent surplus back in 2007. China cannot rely on global growth the way it did from 1990 to 2010; it is simply too big an economy today. China’s share of global manufacturing is already 30 percent. As seen in Figure 1, China’s manufacturing trade surplus as a share of world GDP is large and has risen rapidly, at almost 2 percent. That is more than the combined share of Japan and Germany’s manufacturing surpluses at their peaks.

Chinese policymakers’ clear preference today is to push manufacturing even further as China’s growth driver, which means taking on an increasingly outsized share of global production – with other countries’ manufacturing sectors needing to shrink to compensate.

China’s size means that its imbalances pose an even greater risk to the global economy. A small economy exports at the world price, but a large one – especially with a dominant market position – can shift global prices and leave the rest of the world to deal with the consequences. When Chinese production is growing faster than its own demand or that of the global economy, the rest of the world cannot absorb China’s increase in manufacturing production without being forced to adjust. These conditions would not appear in a normal, market economy. What we are seeing is a fundamental distortion, driven by government policy.

Imbalances and Overcapacity

China’s large imbalances have spillovers on their own, but China’s non-market policies and practices amplify this effect by distorting markets, undercutting fair competition, and concentrating the spillovers into certain sectors. In particular, the combination of China’s enduring macroeconomic imbalances and large-scale government support to specific industrial sectors drive industrial overcapacity.

The scale of this support is striking: China’s industrial subsidies are simply much larger than those of other countries. The Center for Strategic and International Studies concludes that China spends roughly 5 percent of GDP on industrial subsidies, 10 times as much as the United States, Brazil, Germany, and Japan.[4] In sectors like semiconductors, steel, and aluminum, China alone accounts for between 80 and 90 percent of global subsidies provided to those industries.[5] China’s subsidies are opaque but emerging patterns suggest the size of subsidies in China is only increasing, especially at local and provincial levels. State-supported investment is surging to strategically important industries and companies, and there are new tools to steer commercial activities, including the use of structural monetary policy tools to advance industrial policy objectives. The central government, local governments, state-owned firms, and the private sector all play a key role in furthering the government’s industrial policy agenda.

Notably, “Government Guidance Funds” or “Government Investment Funds” continue to use public resources to make equity investments in industries and activities that the Government considers important, with very limited transparency. Academic studies estimate these funds have provided more than $1 trillion in capital and guarantees to over 28,000 mostly private companies from 2000 to 2018.[6] One of these government guidance funds – of which there are over 2,000 at the national and subnational levels – specifically targets the semiconductor sector and is larger than the entire CHIPS & Science Act. Other large-scale initiatives, including the “Little Giants” and “Single Champion”, demonstrate that China’s private sector does not solely operate through market forces – but rather benefit from the network of government guidance funds, state-owned banks, and SOEs who serve as financiers and customers to private firms.

These practices channel China’s vast savings into certain sectors, as directed by Beijing. China’s “Made in China 2025” was launched in 2015 to promote certain strategic sectors. As seen in Figure 2, China has successfully promoted the exports of and discouraged imports of “strategic sectors” as defined by the 2015 policy, with notable results. Imports have been falling as a share of China’s economy, but even more in strategic sectors. And, while non-strategic sector exports fell as a share of China’s economy, exports in strategic sectors grew.

Today, China’s push on manufacturing to drive growth is translating to an apparent surge in lending to industrial sectors, mirroring a decline in lending to real estate sectors (Figure 3). At the same time, growth in China’s export volumes is rising faster than total export values (calculated in USD), rising 11.5% versus 1.5%, respectively, in the first quarter of 2024 compared to the previous year. Increases in export volume were particularly high for electric vehicles (+20%), solar batteries (+30%), and semiconductors (+25%), while overall export prices have fallen significantly since the beginning of 2023.

In today’s interconnected economy, such overcapacity can also lead to the concentration of supply chains in ways that ultimately reduce economic resilience. As evidenced by the personal protective equipment (PPE) supply chain disruptions during the pandemic, significant concentrations of supply chains in a single country increases the risks of disruptions. We see sectors such as solar panel manufacturing, critical minerals processing, permanent magnets, that are heavily concentrated in China. This is not just an issue for the United States or other advanced economies, emerging markets have seen their import concentration from China increased in recent years.[7]

Defining Overcapacity

But what do we as policymakers mean when we talk about Chinese overcapacity? Defined most simply, it is production capacity in excess of domestic demand and untethered from global demand – and we are concerned about the patterns of overinvestment and state support driving it. While periodic surpluses can occur within natural business cycles, we are concerned about structural overcapacity, which stems from persistent patterns of overinvestment and is facilitated by extensive state support.

There is no single test or condition that indicates overcapacity. We cannot simply put in a few statistics about a sector and get a thumbs up or down of whether overcapacity exists. Instead, I will outline three sets of indicators, or “warning signs.”

The first metric is whether expansion in production capacity is growing faster than even the most ambitious demand projections.

The second is rate of lossmaking and inefficient firms. The widespread presence of such firms reflects limited or slow adjustment to changing market conditions and a deteriorating ability to translate investment into revenue. Rising production and investment alongside these indicators would suggest overcapacity.

And third, low or sharply declining capacity utilization rates. Sustained low utilization rates strain profitability of firms and imply the existence of surplus capacity.

None of these metrics are definitive or dispositive on their own, and overcapacity can exist without some of these indicators. For example, with enough subsidies, capacity utilization might be quite high despite excess production. But together they provide an analytical foundation for identifying overcapacity. And on each metric, we are seeing persuasive evidence of not only Chinese overcapacity, but the clear link to the policies driving it.

In China’s case, sectoral conditions are exacerbated by non-market policies and practices, which break the link between company behavior and market forces, and enable these companies to sell goods overseas at prices that are below what their market-driven competitors are able to offer. This then enables the company that has benefited from such government support to grow their market share, potentially leading to over-concentration on a few suppliers.

- Supply rising faster than any plausible level of global demand

First, in certain sectors, Chinese capacity is rising faster than any plausible level of global demand (Figure 4).

For example, China’s production capacity in lithium-ion batteries and solar modules is set to exceed projected global demand by 2 to 3 times over the next few years compared to what is necessary to achieve a path to net-zero emissions by 2050.[8] Similarly, China’s planned production capacity for EVs in 2030 is set to reach over 70 million vehicles, while global EV sales are estimated to only reach 44 million in that year. [9] These figures rely heavily on projections of future supply and demand, which may change. We are assuming that demand will not rise more rapidly than needed under net-zero scenarios. If global prices were to decline due to falling Chinese export prices, demand for Chinese goods would rise, but such low prices would likely eliminate production outside China.

2. More lossmaking and inefficient firms

Second, though the presence of lossmaking firms and low returns to investment can be natural in new or transforming industries, the presence of lossmaking firms in China is found even among mature industries. Firms losing money should go out of business, not continue producing and adding to supply. But, if subsidies or other support from government (including local governments loathe to see an industry leave its borders) prop the firm up, it can stay in business far longer.

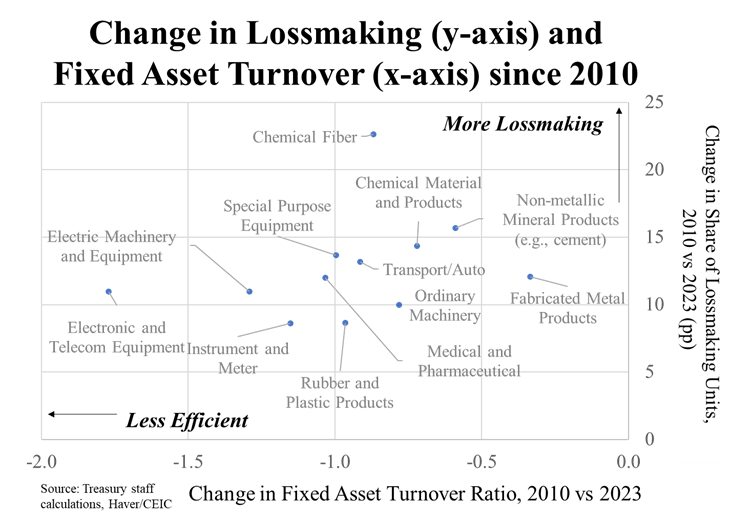

The share of lossmaking industrial firms in China is at its highest level in recent years, and the total number of lossmaking industrial firms is at its highest point since the 1990s, as seen in Figure 5.[10] Further, indicators of capital efficiency have declined over the past ten years across all sub-sectors with available data (Figure 6).

Lossmaking is especially pronounced in China’s auto industry. The share of publicly-traded loss-making firms in the auto industry was 28 percent, outpacing the economy-wide average of 20 percent in 2022. Within the subset of Chinese EV manufactures, only a handful are currently profitable, and these few firms are now facing intense margin pressure.[11]

3. Low or Declining Capacity Utilization

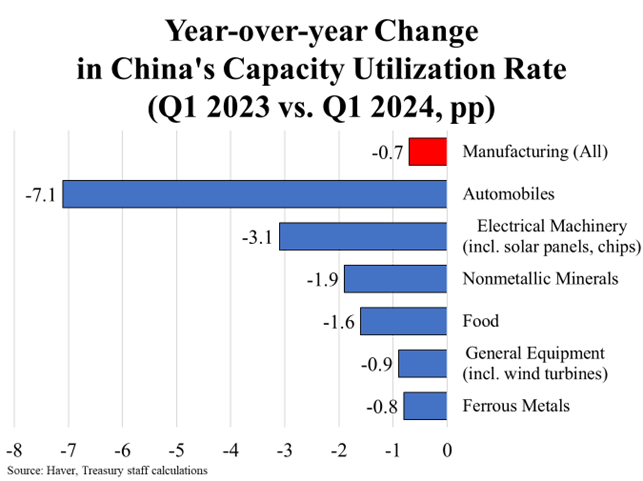

And the third metric is low or declining rates of capacity utilization. Of course, capacity utilization rates can fluctuate with the business cycle, but that cannot fully explain the consistently low rates seen in many of the Chinese manufacturing sectors. Data from the first quarter of 2024 shows China’s manufacturing capacity utilization rate has fallen to its lowest point since 2016 at 73.8% (Figure 7), while the capacity utilization rate of OECD countries typically has remained around 80%.[12]

This decline was particularly pronounced for sectors that Beijing prioritizes, including in automobiles, solar panels, and semiconductors (Figure 8). Utilization rates for finished solar panel production tumbled to 23% in February 2024, down from more than 60% a year earlier.[13] And the IEA estimates that last year, China’s battery output was less than 50% of total production capacity.[14]

For cars, China’s capacity utilization rates have exhibited a consistent downward trend since its 2017 peak of nearly 85% and fell to 65% in the first quarter of 2024, even while auto production increased.[15] While top companies such as BYD are reportedly operating at above 80%, analyst reporting showed the average capacity utilization rate for new energy vehicles in 2023 was less than 50%.[16]

China’s Actions and Counter Argument

Some Chinese officials have argued publicly that other economies have production in excess of domestic demand and this is a normal part of trade. As I said earlier, our concern is not about exports or even Chinese firms having a comparative advantage in some areas. It is that the breadth of China’s government support means that production does not respond to global market demand. The United States and many other market economies have successful export sectors, but our firms have incentives to respond to market signals. During a global downturn, adjustment falls first and foremost on market economies.

Chinese firms guided and supported by the government will expand production, face domestic market saturation, and then resort to exporting excess production at below-market prices. Chinese production is also less responsive during a downturn. Rather than decreasing production or undergoing industry consolidation, Chinese industries can often maintain production, pushing excess supply abroad. In both cases, the results are similar: overcapacity distorts global prices, threatens the long-term viability of foreign competitors, and shifts adjustment onto foreign countries, advanced and developing economies alike. Another helpful indicator of overcapacity is how other countries are responding. Rising cases of antidumping being brought against firms from a particular country may suggest that its firms are selling at prices below cost or normal market conditions.

Chinese government support comes from a broad range of government bodies. We have seen time and time again examples of Beijing announcing a new priority, and then the state actors across the country rushes to support it. This will mean central government, provincial, or city-level support, amplified by state owned banks, for that locality’s specific champion or champions, leading to a rapid and broad-based expansion of production in that politically important sector.

Tools for Responding to Overcapacity Concerns

China’s imbalances and their spillovers have not gone unnoticed – Secretary Yellen has consistently raised China’s unfair economic practices and overcapacity concerns with her counterparts, from her first visit to Beijing last year to their recent meetings in April. The Biden Administration has taken important steps to level the playing field, using a range of tools to protect American manufacturers who are subject to unfair and heavily subsidized competition. This includes ongoing diplomatic engagement with Chinese counterparts, including through the Economic Working Group; historic investments under the CHIPS Act, the Bipartisan Infrastructure Law, and the Inflation Reduction Act; and trade enforcement, including the revised Section 301 tariffs or actions involving anti-dumping or countervailing duties.

The results of the Section 301 review outlined strategic and targeted steps that are needed to respond to specific long-standing unreasonable trade practices related to forced technology transfer by China. In crafting the tariff regime to achieve this objective, President Biden directed USTR to raise tariffs on $18 billion of imports in sectors where we are looking to preserve and increase supply chain resilience and protect American workers in the face of unfair Chinese production. Along with our interagency colleagues, we will continue to monitor and respond to China’s use of non-market policies and practices and use the tools at our disposal to secure fair competition.

We are not isolated in seeking to address negative spillovers from China’s non-market practices. The EU and Turkey have also recently imposed tariffs on Chinese EV imports; Mexico, Chile, and Brazil have taken trade actions on Chinese steel; and India uses tariffs and other trade tools to defend its solar manufacturers from Chinese dumping. And while each country had their own concerns and needs, the underlying reason is undeniable. As the G7 Leaders and Finance Ministers have stated – China’s overcapacity “undermines our workers, industries, and economic resilience and security.” The United States will act, and we won’t be alone.

Conclusion

Let me conclude with a broader perspective.

First, overcapacity concerns are not new, and China is not blind to them. In the past, China has acknowledged excess capacity in several industries, including steel, cement, and glass. And more recently, Chinese officials have publicly acknowledged overcapacity as a risk to sustained economic recovery during their Congress’s annual meetings in March and their Central Economic Work Conference last December. Continued production beyond what a market can bear is an inefficient waste of resources. Reigning in overcapacity could be good for China, boosting productivity and efficiency. However, their efforts from prior years to address overcapacity in a small number of sectors are being reversed, and overcapacity is clearly growing.

Second, this a global issue. The United States, along with our allies and partners in developing economies and advanced economies alike, share mutual objectives to address China’s policies that have negative economic spillovers to our firms, workers, and economic resilience.

Third, addressing these challenges may warrant our taking defensive action to protect our firms and workers – and the traditional toolkit of trade actions may not be sufficient. More creative approaches may be necessary to mitigate the impacts of China’s overcapacity. We should be clear: defense against overcapacity or dumping is not protectionist or anti-trade, it is an attempt to safeguard firms and workers from distortions in another economy.

The best outcome, though, would be for China to acknowledge the growing concerns among its major trading partners and work with us to address them. We will take defensive action if needed, but we would prefer for China to take action itself to address the macroeconomic and structural forces that are generating the potential for a second “China shock” for its major trading partners. China could boost consumption by strengthening its safety net, increasing household incomes, reforming its internal migration rules. It could better support services, not just manufacturing. It could reduce harmful and wasteful subsidies. These would all be in China’s interest and reduce tensions.

As I described earlier, the Treasury Department has shared these concerns through regular engagements with our Chinese counterparts. We have advocated for specific steps to ensure American workers and firms are treated fairly, and we will continue to work bilaterally toward a healthy economic relationship that benefits both countries.

Thank you.

###

[1] Suntech, Owing Millions, Faces a Takeover. NYT, March 2013.

[2] World Steel Association.

[3] Bureau of Labor Statistics.

[4] Red Ink: Estimating Chinese Industrial Policy Spending in Comparative Perspective (csis.org), and Big Spender – The Wire China

[5] Government support in industrial sectors: A synthesis report | en | OECD

[6] Government as an Equity Investor: Evidence from Chinese Government Venture Capital through Cycles by Jinlin Li :: SSRN

[7] Rhodium Group, How China’s Overcapacity Holds Back Emerging Economies

[8] BloombergNEF

[9] China’s EV overcapacity spurs global fears of more price cuts – Nikkei Asia

[10] National Bureau of Labor Statistics.

[11] Li Auto Profit Fell on Higher Operating Expenses. WSJ, May 2024

[12] China National Bureau of Statistics, Trading Economics.

[13] China solar industry faces shakeout, but rock-bottom prices to persist | Reuters

[14] Global EV Outlook 2024 (iea.blob.core.windows.net), pg.81.

[15] CEIC via Haver

[16] China’s underutilized factories fan export dump fears in U.S. and Europe – Nikkei Asia.

Figure 1.

Figure 2.

Figure 3.

Figure 4.

Figure 5

Figure 6

Figure 7

Figure 8

Official news published at https://home.treasury.gov/news/press-releases/jy2455

{kind=link}